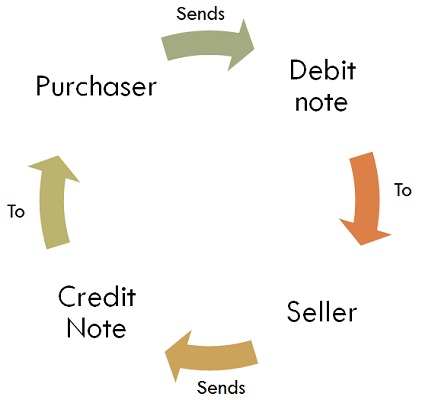

Millions of purchase and sale transactions occur in day to day life, and so does the returns are made by many customers, when they find the products are not up to their requirement. Debit Note and Credit Note are used while the return of goods is made between two businesses. Debit Note is issued by the purchaser, at the time of returning the goods to the vendor, and the vendor issues a Credit Note to inform that he/she has received the returned goods.

When the goods are returned to the seller or supplier, a debit note is issued to him which indicates that his/her account has been debited with the respective amount. On the other hand, when a customer returns goods, a credit note is issued to him which shows that his account has been credited with the amount indicated in the note. Here in the given article, we have discussed the substantial differences between a debit note and credit note, take a read.

Content: Debit note Vs Credit Note

- Comparison Chart

- Definition

- Key Differences

- Conclusion

Comparison Chart

| BASIS FOR COMPARISON | DEBIT NOTE | CREDIT NOTE |

|---|---|---|

| Meaning | Debit Note is a document which reflects that a debit is made to the other party's account. | Credit Note is an instrument used to inform that the other party's account is credited in his books. |

| Use of | Blue Ink | Red Ink |

| Represents | Positive Amount | Negative Amount |

| Which book is updated on the basis of note? | Purchase Return Book | Sales Return Book |

| Effect | Minimization in account receivables. | Minimization in account payables. |

| Exchanged for | Credit Note | Debit Note |

Definition of Debit Note

A commercial instrument made and issued by the purchaser and delivered to seller giving details regarding the amount debited from the seller’s account and the reasons for the same is known as Debit Note. The document provides information to the vendor that a debit has been made to his account in the buyer’s book. The reasons for debiting the account are given as under:

- When the buyer’s account is overcharged, he sends a debit note to seller.

- When the buyer returns the goods purchased by him, then also he delivers the debit note.

- When the buyer undercharges the seller’s account, then he issues debit note.

The seller issues a credit note to the buyer as an acknowledgment of the Debit Note. It is written in blue ink. In general, Debit note reduces the receivables.

Definition of Credit Note

A memo prepared and issued by one party to the other party, containing the details of the amount credited to the buyer’s account and the reasons for so, is known as Credit Note. It is issued in exchange for the Debit Note. It gives the information to the buyer; that is account is credited in the vendor’s book. The note is prepared with red ink. The reasons for issuing a credit note is as under:

- When the buyer overcharges the seller’s account, the issues the credit note.

- When the supplier gets back the goods sold by him to the buyer, then also credit note is issued.

- A buyer can also send credit note, in case the seller undercharges him.

The issue of credit note shows that the account payables are reduced. In general, it shows the negative amount.

Key Differences Between Debit Note and Credit Note

The following are the differences between debit note and credit note:

- A memo sent by one party to inform the other party that a debit has been made to the seller’s account, in buyer’s books, is known as Debit Note. A commercial document which is sent by one party to inform the other party that a credit has been made to buyer’s account, in seller’s books is known as Credit Note.

- Debit Note is written in blue ink while Credit Note is prepared in red ink.

- Debit Note is issued in exchange for Credit Note.

- Debit Note represents a positive amount whereas Credit Note prepares negative amount.

- Debit Note reduces receivables. On the other hand, Credit Note reduces payables.

- On the basis of the Debit Note, purchase return book is updated. Conversely, sales return book is updated with the help of a Credit Note.

The following are the differences between debit note and credit note:

- A memo sent by one party to inform the other party that a debit has been made to the seller’s account, in buyer’s books, is known as Debit Note. A commercial document which is sent by one party to inform the other party that a credit has been made to buyer’s account, in seller’s books is known as Credit Note.

- Debit Note is written in blue ink while Credit Note is prepared in red ink.

- Debit Note is issued in exchange for Credit Note.

- Debit Note represents a positive amount whereas Credit Note prepares negative amount.

- Debit Note reduces receivables. On the other hand, Credit Note reduces payables.

- On the basis of the Debit Note, purchase return book is updated. Conversely, sales return book is updated with the help of a Credit Note.

0 Comments

Thanks for comment your feedback more valuable.